OpenAI Raises $110 Billion: Analysis of a Historic Turning Point for AI

On February 27, 2026, OpenAI closed the largest fundraising round in tech history. With Amazon, NVIDIA, and SoftBank as investors, the valuation reaches $840 billion. Full analysis: context, competitive impact, LLM API market, risks, and 2026-2027 outlook.

Updated

OpenAI Raises $110 Billion: Analysis of a Historic Turning Point for AI

OpenAI's $110 billion fundraising round, announced on February 27, 2026, represents far more than a financial record. It is a structural signal about the state and direction of the artificial intelligence industry, an unprecedented concentration of capital in the history of technology, and an event that rewrites the rules of the game for every entrepreneur, developer, and decision-maker who uses or considers using AI in their business. OpenAI, the company behind ChatGPT, closed this round with a post-money valuation of $840 billion, positioning itself among the most valued companies on the planet, ahead of giants like TSMC or Berkshire Hathaway.

But beyond the staggering numbers, what does this operation concretely mean for the tech ecosystem, for competitors like Google, Anthropic, or Mistral, for the LLM API market, and above all for you as an entrepreneur or developer?

Key Figures

| Metric | Value |

|---|---|

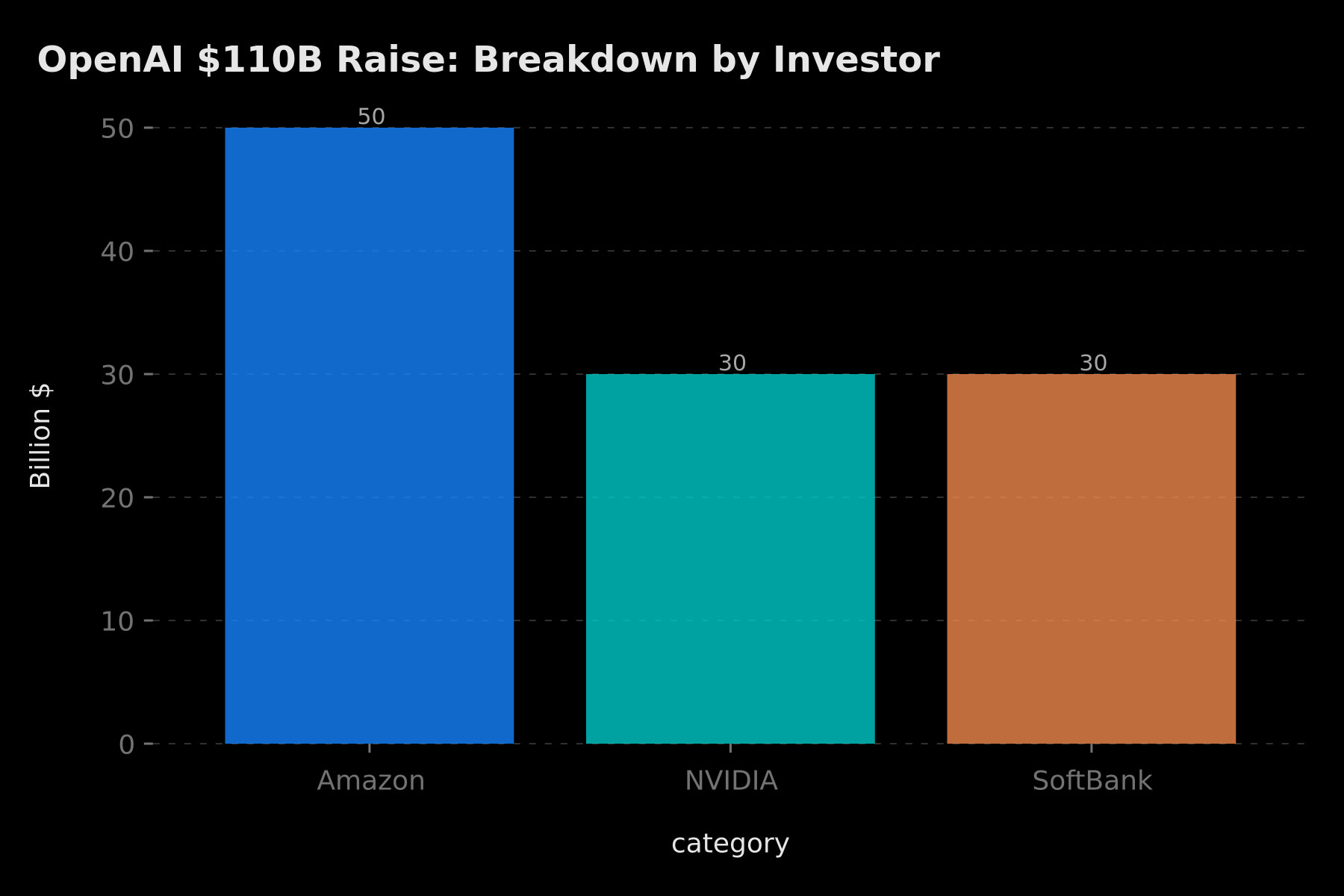

| Amount raised | $110 billion |

| Pre-money valuation | $730 billion |

| Post-money valuation | $840 billion |

| Lead investor | Amazon ($50B) |

| Major co-investors | NVIDIA ($30B), SoftBank ($30B) |

| Weekly ChatGPT users | 900 million |

| 2025 revenue | $13 billion |

| 2026 revenue target | $20 billion |

| Anticipated cash burn by 2029 | $218 billion |

Amazon $50B, NVIDIA $30B, SoftBank $30B

Amazon $50B, NVIDIA $30B, SoftBank $30B

Why Amazon Invests $50 Billion

Amazon's massive investment isn't just a financial bet. It's a deep strategic partnership that fits into the logic of the AI infrastructure war. To understand Amazon's decision, it must be placed in its competitive context: Microsoft had taken a considerable lead by investing $13 billion in OpenAI in 2023, integrating GPT-4 across its entire Microsoft 365 suite and Azure. Amazon, whose AWS represents roughly a third of the global cloud market, could not afford to sit on the sidelines while its primary competitor built a durable competitive advantage through AI.

- Cloud infrastructure: AWS becomes a primary cloud provider for training and inference of OpenAI models, complementing Microsoft Azure. This means millions of GPT API calls will route through Amazon's servers, generating direct revenues for AWS.

- Alexa integration: GPT models could power Amazon's next generation of voice assistants. Alexa, long criticized for its limitations compared to more recent AI assistants, would benefit from a radical upgrade.

- Augmented e-commerce: Integrating advanced conversational capabilities into the Amazon marketplace would transform the shopping experience: personalized recommendations, product comparisons in natural language, world-class AI customer support.

- Insurance against dependency: By combining its investments in Anthropic (via AWS) and now OpenAI, Amazon positions itself as the neutral AI platform — one that wins regardless of which technology ultimately dominates.

In our analysis, Amazon's investment is also a defensive decision: by funding OpenAI, Amazon secures preferential access to the technology, favorable commercial terms for AWS, and influence over the trajectory of a company that could otherwise become a competitor in the AI assistant space for consumers.

NVIDIA: From Chip Supplier to Strategic Investor

NVIDIA's $30 billion reveals a paradigm shift in Jensen Huang's strategy. NVIDIA is historically a hardware seller — primarily GPUs — that derives its value from chip sales volume. But as AI became the primary growth engine of the tech industry, NVIDIA understood that investing in its largest chip consumers created a virtuous value loop.

- Virtuous cycle: The more OpenAI grows, the more NVIDIA H100 and H200 chips it purchases, justifying the investment and maximizing financial returns.

- Hardware/software co-development: NVIDIA and OpenAI co-optimize hardware architectures for next-generation models. The new Blackwell Ultra GPUs, whose roadmap coincides with OpenAI's expansion plans, are partly dimensioned for the specific needs of large language models.

- Industry standard: By funding both sides of the AI value chain (hardware + software), NVIDIA consolidates its de facto monopoly on AI infrastructure, making alternatives like Google TPU chips or AMD MI300 processors structurally less attractive.

NVIDIA's strategy echoes Intel's in the 1990s: by becoming indispensable to the entire chain, the company captures a disproportionate share of the value created by the industry. In our reading, the OpenAI investment reinforces this dynamic for the next five years.

SoftBank and the Long-Term Vision

The $30 billion invested by SoftBank deserves particular attention, as it follows a different logic from Amazon or NVIDIA. Masayoshi Son, SoftBank's founder, built his fortune on long-term tech bets (Alibaba, Sprint, WeWork — with mixed results). In our analysis, the OpenAI investment represents SoftBank's attempt to reposition itself after the Vision Fund's setbacks around overvalued valuations.

SoftBank's interest is threefold: first, access to the world's most advanced AI for its tech company holdings across Asia and Europe. Second, the possibility of creating synergies with Arm Holdings — of which SoftBank remains the principal shareholder — to develop specialized AI chips. Third, restored credibility with institutional investors after Vision Fund losses, by associating with what is now considered the most strategically valuable tech asset in the world.

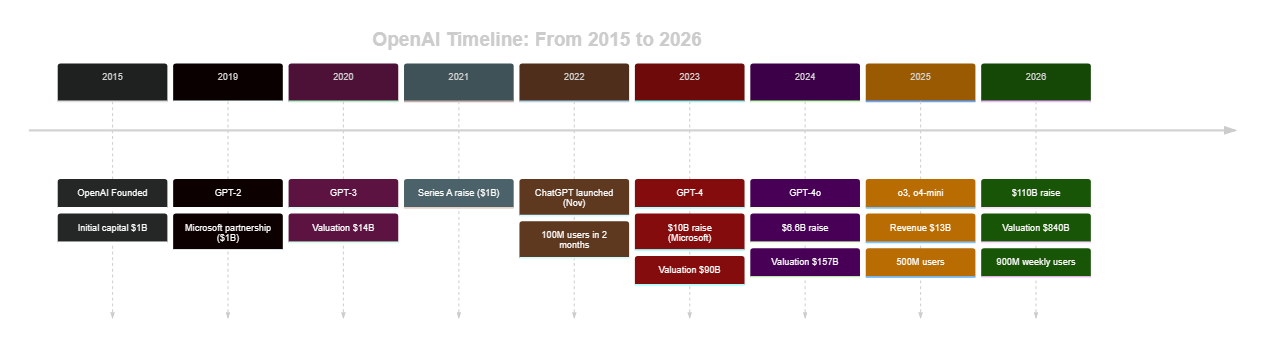

The OpenAI Timeline: A Meteoric Rise

To measure the magnitude of this turning point, it's useful to trace OpenAI's trajectory since its founding:

OpenAI evolution: from nonprofit startup in 2015 to $840B valued company in 2026

OpenAI evolution: from nonprofit startup in 2015 to $840B valued company in 2026

OpenAI was founded in 2015 as a nonprofit with $1 billion in capital commitments, including from Elon Musk and Peter Thiel. The first Microsoft partnership in 2019 ($1 billion) marked the beginning of commercialization. GPT-3 in 2020, then ChatGPT in November 2022, changed the trajectory: 100 million users in 2 months, a record that has never been approached in the history of consumer applications. The Microsoft raise of $10 billion in 2023 at a $90 billion valuation was followed by a $6.6 billion raise in 2024 at $157 billion. In less than 18 months, the valuation was multiplied by more than 5.

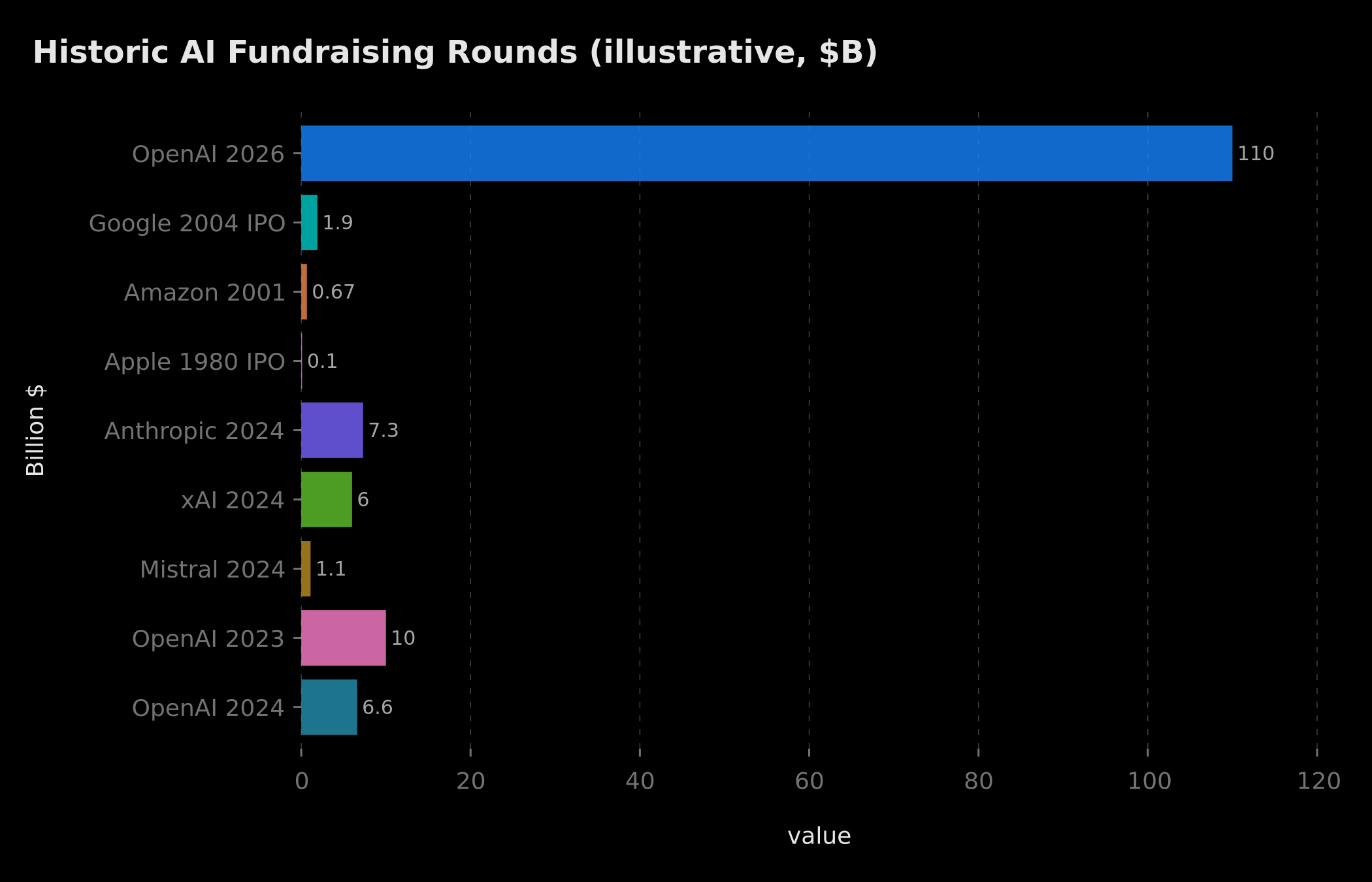

The OpenAI Raise Compared to Historic Tech Fundraising

To contextualize the magnitude of this operation, in our analysis it is instructive to compare it to the great raises and IPOs that have marked tech history:

OpenAI's $110B represents 10x Microsoft's 2023 OpenAI investment, and dwarfs historic IPOs from Google, Amazon, or Apple — illustrative data

OpenAI's $110B represents 10x Microsoft's 2023 OpenAI investment, and dwarfs historic IPOs from Google, Amazon, or Apple — illustrative data

The comparison is striking. Google's 2004 IPO raised $1.9 billion. Amazon's 1997 IPO raised approximately $54 million. Apple raised $100 million in its 1980 IPO. Even the largest recent raises by AI players — Anthropic at $7.3 billion in 2024, Elon Musk's xAI at $6 billion, Mistral at $1.1 billion — appear modest compared to OpenAI's $110 billion. This concentration of capital in a single private entity is, in our reading, unprecedented in the history of technological capitalism.

What makes the comparison even more striking: Google, Amazon, and Apple raised these amounts at their public offerings, with full investor liquidity. OpenAI remains a private company — albeit with a complex hybrid structure between a nonprofit and a commercial entity — meaning investors are betting on future liquidity (IPO or acquisition) at even higher valuations.

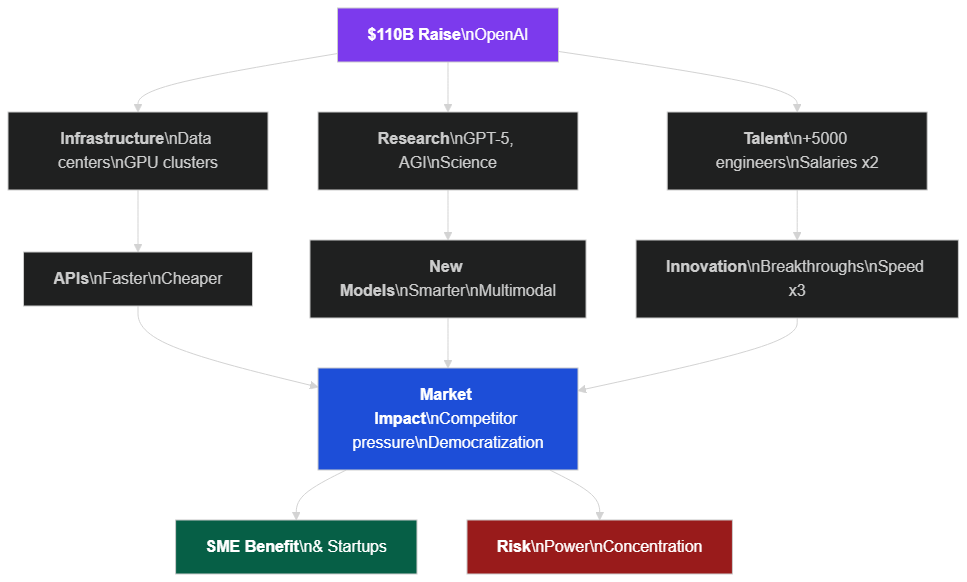

What $110 Billion Enables OpenAI to Do

Next-Generation Infrastructure at Scale

The first major expenditure will be infrastructure. Training a model like GPT-5 requires thousands of H100/H200 GPUs running for months, at an estimated cost between $500 million and several billion dollars depending on model scale. With $110 billion, OpenAI can plan not one but several next-generation datacenter clusters, in parallel rather than in sequence.

The AWS agreement accelerates this deployment by using Amazon's existing infrastructure as a substrate while building dedicated capacity. In our analysis, this means model training timelines could be drastically compressed, potentially shrinking from 6-12 months to a few weeks for certain architectural types.

Impact chain: infrastructure → models → APIs → SME benefits and power concentration risks

Impact chain: infrastructure → models → APIs → SME benefits and power concentration risks

Fundamental Research and the AGI Race

OpenAI has explicitly indicated that funds will support research toward AGI (Artificial General Intelligence). In our reading, this is the most significant signal from this raise: the company isn't merely looking to improve ChatGPT at the margin, it's accelerating its trajectory toward what it considers the ultimate goal of AI. This includes research into multi-step reasoning, more sophisticated reinforcement learning from human feedback (RLHF), and hybrid architectures combining the strengths of LLMs with other computational paradigms.

Talent: The Brain War Intensifies

With financial resources of this magnitude, OpenAI can offer unprecedented compensation packages. Senior ML engineers, already courted by Google, Meta, DeepMind, and Anthropic, now see salaries exceeding $1 million annually. In our analysis, this creates an inflationary dynamic across the entire AI labor market: even startups and SMEs using AI developers see their salary costs rise through a cascade effect.

Impact on Competition: Google, Anthropic, Mistral, and xAI Under Pressure

OpenAI's raise reshuffles the competitive AI landscape at multiple levels. Here's how the main players are responding according to our reading of market dynamics.

Google remains the best structurally positioned competitor: its own TPU chips, proprietary data from Search, and its Gemini Ultra model progressing rapidly. But Google faces double pressure — needing to invest massively in AI to defend its core business (Search is threatened by AI assistants) while managing the profitability expectations of stock market shareholders. OpenAI's raise forces Google to accelerate its deployments, which can lead to errors and reputation incidents like the Gemini affair in 2024.

Anthropic, founded by former OpenAI employees including Dario and Daniela Amodei, raised $7.3 billion in 2024 with Amazon as its lead investor. The irony is that the same Amazon now invests $50 billion in its direct competitor. In our analysis, Anthropic must now demonstrate that its differentiated value proposition — AI safety and Claude's reliability — can justify market share in an environment where OpenAI has 15 times more resources. Its decision to refuse a deal with the Pentagon, unlike OpenAI, has also excluded it from lucrative government contracts.

Mistral AI, the French startup, finds itself in an extreme asymmetric position. With its $1.1 billion raised, Mistral bets on efficiency: smaller, faster models, deployable on-premise, which appeal to European companies concerned about data sovereignty. It's a viable niche strategy, but OpenAI's raise means GPT-4 level models will likely become open-source or near-free within the next 18 months, which could reduce Mistral's competitive advantage.

xAI by Elon Musk (creator of Grok) raised $6 billion in 2024. Musk's strategy relies on integration with X (formerly Twitter) and access to unique real-time data. But facing OpenAI's $110 billion, xAI finds itself structurally undercapitalized for the race toward large foundation models.

900 Million Users: A Game-Changing Number

According to data published by OpenAI, ChatGPT now has 900 million weekly active users. To put this in perspective:

- That's 3 times more than a year ago

- It's the fastest-growing application in history

- 9 million business users pay for a subscription

- Codex (code assistant) usage tripled to reach 1.6 million weekly users

These numbers show that AI is no longer a niche toy. It's a daily production tool for hundreds of millions of people. In our analysis, the critical mass reached by ChatGPT creates a powerful network effect: the more the tool is used, the more feedback data improves the models, the more models attract new users. This cycle is difficult for competitors to break, even well-funded ones.

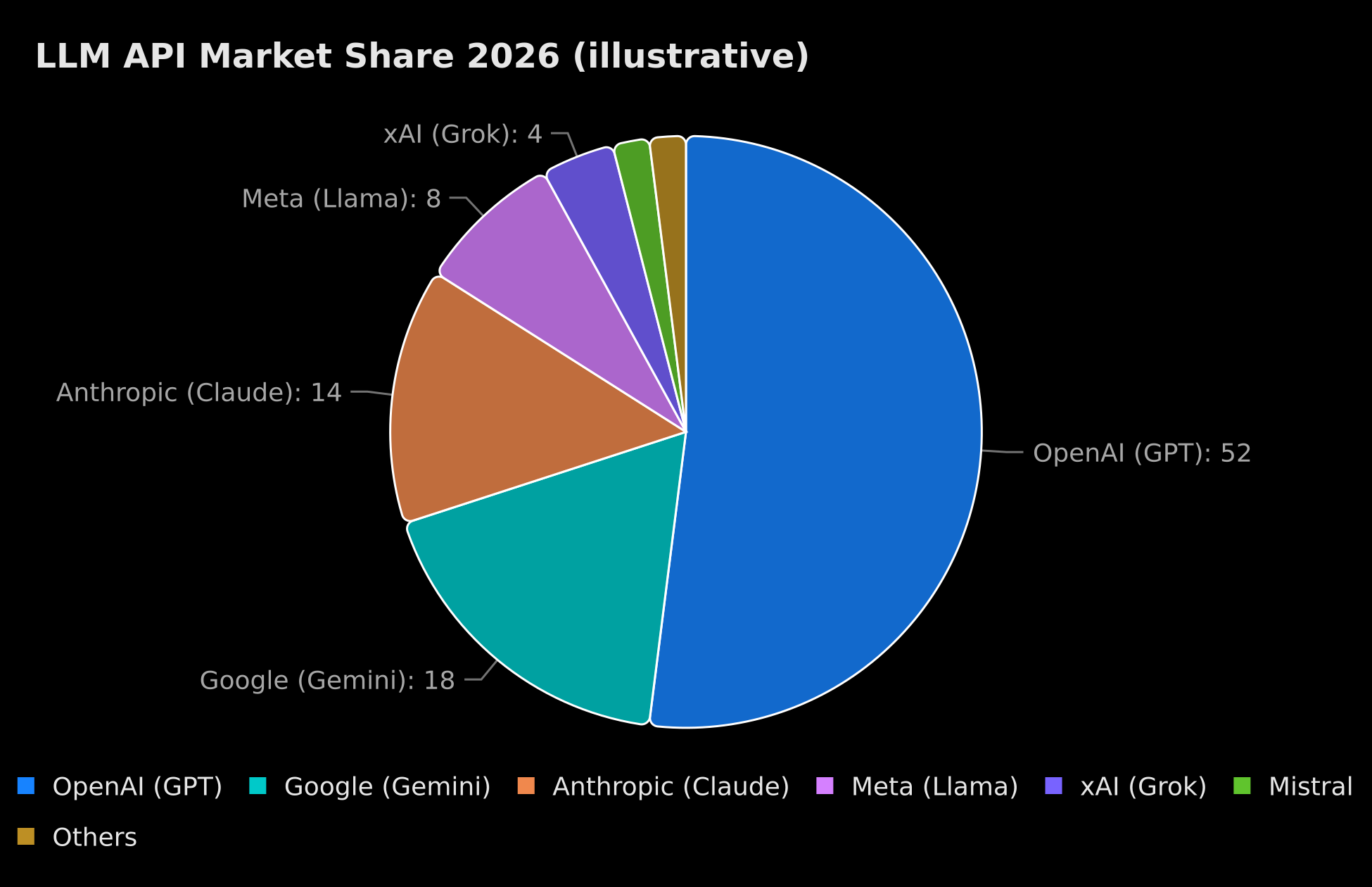

Impact on the LLM API Market: Pricing, Availability, and Developers

The LLM API market — the programmatic interfaces that allow developers to integrate OpenAI's intelligence into their applications — is directly affected by the fundraise. Based on our reading of historical dynamics, several trends are emerging.

OpenAI dominates with ~52% of the LLM API market, followed by Google Gemini (~18%) and Anthropic Claude (~14%) — illustrative data

OpenAI dominates with ~52% of the LLM API market, followed by Google Gemini (~18%) and Anthropic Claude (~14%) — illustrative data

Price drops: The economies of scale enabled by $110 billion in capital should continue pushing API prices down. Between 2022 and 2025, GPT API call costs were divided by 100 for standard use cases. In our analysis, this trend will continue: prices could fall another 50-70% by 2027, making advanced AI accessible to applications and budgets currently excluded from the market.

Improved SLAs: Massive resources allow OpenAI to improve availability, response times, and service guarantees. For entrepreneurs who have integrated GPT into critical products, this is excellent news — the risk of outages or performance degradation decreases significantly.

Pressure on open-source alternatives: The massification of OpenAI's resources makes proprietary models so powerful and accessible that it questions the value of self-hosting open-source models like Llama or Mistral. For cost-conscious developers, the "build vs. buy" question is constantly revisited.

To explore how these dynamics intersect with the war between open and closed models, our analysis of DeepSeek V4 vs GPT-5.5 provides indispensable complementary insight.

Implications for Entrepreneurs and Developers

AI as a Production Commodity

With investments of this magnitude, the cost of accessing AI models will continue to fall. OpenAI APIs will be faster, more reliable, and potentially cheaper. For startups and SMEs, this is a structural opportunity: you can integrate world-class AI into your products without investing billions. The real question is no longer "can we afford AI?" but "which AI do we integrate and how?"

If you want to understand AI-related investments in the startup world, our article on why 68% of funded startups have AI at their core strategy details current investment trends shaping the market.

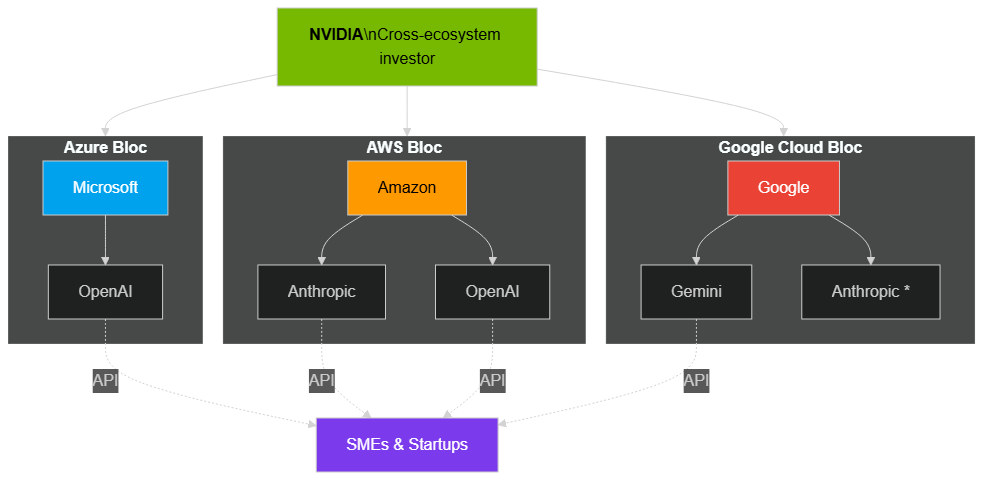

The Ecosystem War: Choosing Your Bloc

The landscape is crystallizing around three blocs that now correspond to three cloud offerings:

- Microsoft + OpenAI (Azure): Best integration with Microsoft 365, GitHub Copilot, and the entire Microsoft ecosystem. Ideal for companies already in the Microsoft universe.

- Amazon + Anthropic + OpenAI (AWS): The most neutral platform, offering access to both leading technologies. Ideal for teams who want flexibility and vendor independence.

- Google + Gemini (Google Cloud): The advantage of integration with Search, Maps, YouTube, and the entire Google ecosystem. Powerful for multimodal use cases.

Choosing your AI provider now also means choosing your cloud provider. Companies must anticipate these alliances to avoid vendor lock-in. Migrating from Azure to AWS today costs 10-20 times less than it will in 5 years once dependencies accumulate.

AI alliance map: Microsoft/OpenAI, Amazon/Anthropic/OpenAI, Google/Gemini — with NVIDIA as a cross-ecosystem investor

AI alliance map: Microsoft/OpenAI, Amazon/Anthropic/OpenAI, Google/Gemini — with NVIDIA as a cross-ecosystem investor

Cash Burn: A Sustainable Model?

OpenAI anticipates cash consumption of $218 billion by 2029. This is an astronomical figure that reminds us that generative AI is a capital-intensive industry. The question remains open: when will OpenAI become profitable? With $13 billion in 2025 revenue and a $20 billion target for 2026, the trajectory is promising, but infrastructure and research costs are growing almost as fast as revenues.

For entrepreneurs, this signal is important: if OpenAI isn't yet profitable despite 900 million users, AI product margins will remain compressed for several more years. Adjust your business models accordingly — and above all, calculate the real cost of integrating an AI chatbot into your product before committing.

Risks: Power Concentration and AI Governance

OpenAI's $110 billion raise raises fundamental governance questions that go far beyond the financial framework. In our analysis, three risks deserve particular attention.

Oligopolistic concentration: When three investors (Amazon, NVIDIA, SoftBank) collectively hold major influence over the company that owns the world's most-used AI, legitimate questions arise about the direction this technology is heading. OpenAI's decisions — on pricing, availability, permitted uses, model transparency — affect hundreds of millions of people without any democratic oversight mechanism.

OpenAI's hybrid governance: OpenAI has a unique and complex legal structure — a "capped profit" entity controlled by a nonprofit association. This structure, designed to keep the AI safety mission above commercial interests, is under increasing pressure as valuations explode. The tension between the original mission (developing AI for humanity's benefit) and the return-on-investment expectations of contributors like Amazon is, in our reading, one of the biggest unresolved questions of this raise.

Accelerating the technology gap: Companies and countries without access to the best AI APIs or the necessary training risk being structurally disadvantaged in an economy where AI becomes basic infrastructure. For entrepreneurs and SMEs, the challenge is not to passively undergo this transformation but to actively participate in it.

To go deeper on AI oversight and control mechanisms, our guide on how to avoid AI hallucinations in enterprise addresses the practical governance mechanisms you can implement at your scale right now.

The Pentagon Deal: AI in Defense

Alongside this raise, OpenAI signed an agreement with the Pentagon to deploy its AI in classified military systems. The agreement includes strict safeguards — prohibition on use for autonomous weapons systems, mandatory human supervision, regular deployment audits. This contract is all the more significant since Anthropic (creator of Claude) refused similar terms, leading to its exclusion from US federal agencies by the Trump administration.

In our reading, this agreement is a commercial decision as much as an ethical one. The defense and government security contract market represents tens of billions of dollars in potential revenues. By accepting these conditions with safeguards, OpenAI secures a competitive advantage in regulated markets that its more cautious competitors won't address.

2026-2027 Outlook: What Will Change

In our analysis, the next 18 to 24 months will see several major evolutions directly linked to this raise.

GPT-5 and beyond: Compute resources will enable training at an unprecedented scale. We expect to see models with long reasoning capabilities, better understanding of long contexts (1 million tokens and more), and much smoother native tool integration (web browsing, code, calculation) than today.

Local inference: Paradoxically, the race toward large foundation models also stimulates innovation on efficient small models. Apple Intelligence, Microsoft Phi-4, and compact Gemini versions show the way: ultimately, models capable of running on your smartphone will offer capabilities equivalent to GPT-3.5 from 2022.

Regulation accelerates: In Europe, the AI Act is entering into force. In the US, the concentration of power around OpenAI will accelerate regulatory discussions. For entrepreneurs, this means the rules around AI usage will evolve — stay informed and build compliant AI systems from the start.

AI for emerging markets: Falling API prices and extending cloud infrastructure across African, Asian, and Latin American markets will create new opportunities. African AI talent is being actively recruited by OpenAI, Google, and Meta, creating a brain drain but also expertise returns and technology transfer opportunities.

Conclusion: The Era of Mega AI Investments

OpenAI's $110 billion fundraise is not merely a financial transaction. It is confirmation that artificial intelligence has entered a new phase — one where states and large corporations treat AI as strategic first-tier infrastructure, on par with energy or telecommunications. Concentrating $110 billion in a single private entity reshapes the competitive landscape, accelerates the AGI race, and raises governance questions that neither markets nor regulators have fully answered.

For entrepreneurs and developers, the message is ambivalent but clear. On one side, unprecedented opportunities: more powerful, cheaper, more reliable APIs. Tools that allow a team of 5 people to build what would have required 50 people five years ago. On the other, growing dependency on a tech oligopoly whose decisions you don't control. AI is no longer a competitive advantage — it's the bare minimum. But how you integrate it, how you govern it, and how you manage dependency on its providers is where your durable competitive advantage will be built.

The most dangerous position you can occupy today is not that of someone who has no AI strategy — it's that of someone who believes they have one without having truly thought through the governance, the costs, and the dependencies it creates. OpenAI's $110 billion raise is a clarion call: the AI era is not coming, it is here, and the companies that thrive will be those that treat AI not as a feature to add but as a strategic foundation to architect with precision, discipline, and adaptability.

At BOVO Digital, we help you integrate AI into your business strategically and deliberately, whether through intelligent chatbots, AI-powered n8n automations, or digital transformation strategies. Contact us for a free audit and discover how to turn this revolution into a concrete advantage for your activity.

Tags

FAQ

Who are the investors in OpenAI's $110 billion fundraising round?

According to information published by OpenAI on February 27, 2026, the three main investors are Amazon ($50 billion), NVIDIA ($30 billion), and SoftBank ($30 billion). These investments reflect deep industrial strategies: preferential access to the most advanced AI technology, integration into their own products, and consolidation of their position in the AI market.

Why is OpenAI's valuation so high at $840 billion?

The $840 billion post-money valuation rests on several pillars: 900 million weekly users, $13 billion in 2025 revenue, a $20 billion target for 2026, and above all the disruptive potential of generative AI across virtually every economic sector. In our analysis, this valuation incorporates a premium for access to AGI technology that far exceeds traditional financial metrics.

How will OpenAI's fundraise affect GPT API pricing?

The $110 billion capital influx will enable OpenAI to massively scale its compute infrastructure and reduce marginal inference costs. Based on our reading of historical trends, GPT API prices should continue to fall 30-50% per year, making advanced AI increasingly accessible to SMEs and independent developers who previously couldn't afford enterprise-grade AI capabilities.

What are the risks of this concentration of power around OpenAI and its investors?

The key risks identified are: structural dependency of businesses on an AI oligopoly (OpenAI + a handful of players), governance questions around a potentially transformative technology, acceleration of the technological gap between large corporations and SMEs, and digital sovereignty issues for countries without national AI champions. Regulators in Europe and Asia are already examining these concentrations under antitrust frameworks.

Will this fundraise accelerate AGI (artificial general intelligence)?

OpenAI has explicitly stated that funds will be partially dedicated to fundamental AGI research. In our analysis, the $110 billion represents massive fuel to accelerate this trajectory. However, timelines remain uncertain: some researchers estimate viable AGI by 2028-2030, while others maintain that fundamental obstacles remain. What is certain is that the capital will compress research timelines across the board.

How can African startups and emerging market companies benefit from this raise?

Massification of AI investments makes OpenAI APIs more accessible and cheaper. For African startups, this means building world-class AI solutions without massive funding. Cloud infrastructure partnerships (AWS, Azure) extending to the continent also reduce latency. The challenge remains connectivity and AI tool training, but the cost barrier to entry is falling dramatically.

Ready to implement this?

Book a free 30-min strategy call with our experts

We'll analyze your situation and propose a concrete action plan.

Déo-Gratias LOKONON

E-Commerce & SEO Expert. Shopify, PrestaShop and digital acquisition strategist. Graduated from Polytech Nantes.